Things To Know Before You Take A Personal Loan For Medical Bills In India

Medical emergencies can strike at any time, and they often come unannounced. For the middle-class population in India, managing the unexpected expenses associated with medical emergencies can be challenging. While health insurance is essential, it may not cover all expenses. In such situations, personal loans can bridge this gap, offering a quick and flexible solution.

To qualify for these loans, individuals typically need to meet certain eligibility criteria, including a stable income and a good credit score. Prerequisites may involve submitting income documents, identity proofs, and address verification. The processing time for these loans is often swift, providing immediate relief during urgent medical situations.

This article will explore personal loans for medical emergencies in India, covering eligibility criteria, prerequisites, processing time, cost, loan quantum, tenor, and a comprehensive analysis of their pros and cons.

To qualify for these loans, individuals typically need to meet certain eligibility criteria, including a stable income and a good credit score. Prerequisites may involve submitting income documents, identity proofs, and address verification. The processing time for these loans is often swift, providing immediate relief during urgent medical situations.

This article will explore personal loans for medical emergencies in India, covering eligibility criteria, prerequisites, processing time, cost, loan quantum, tenor, and a comprehensive analysis of their pros and cons.

Table of content:

- Eligibility criteria

- Prerequisites

- Processing time

- Costs

- Interest rates

- Processing fees

- Prepayment charges

- Late payment fees

- Availing a personal loan based on the type of treatment

- Availing a personal loan based on patient-borrower relationship

- Health insurance coverage

- Pros of using personal loans during medical emergencies

- Cons of using personal loans during medical emergencies

- What to remember before taking a personal loan

- How Milaap can help

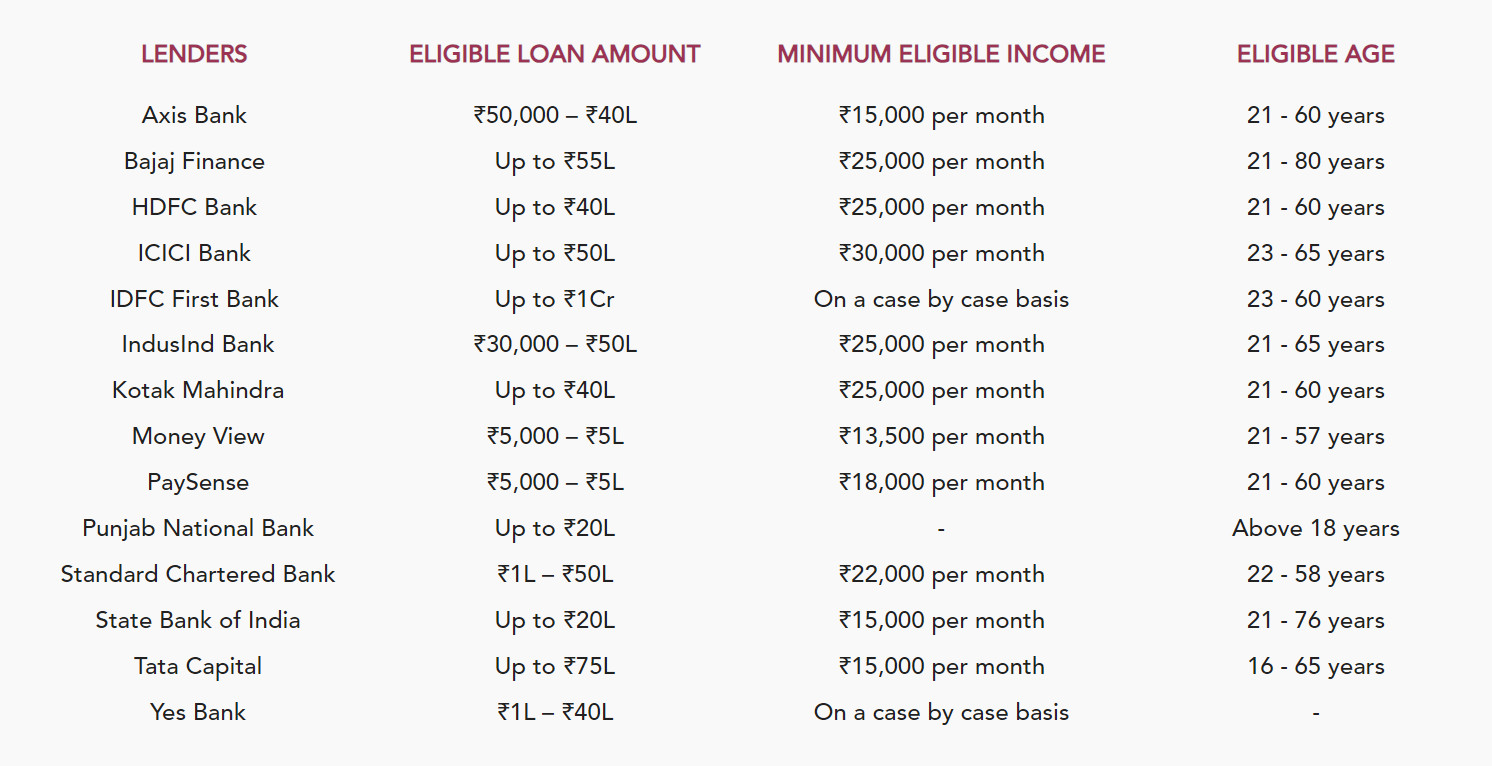

Eligibility criteria

Understanding these criteria is crucial for potential borrowers, as they provide insights into the factors lenders consider when evaluating eligibility for personal loans. Meeting these requirements enhances the likelihood of a successful loan application.

For self-employed applicants

For salaried applicants

- Age limit: Applicants should typically be between 18 and 60 years old to be eligible for a personal loan as a salaried individual. Some banks offer loans to applicants aged more than 60 as well.

- Minimum income: A minimum monthly income, often around ₹15,000 – ₹ 25,000, is required. However, this figure may vary depending on the lending institution.

- Minimum work experience: Typically, a minimum work experience of 1 year is preferred, though some lenders may require a longer tenure of employment.

- Credit score: Salaried applicants are generally expected to have a credit score of preferably 700 and above for a higher chance of loan approval.

For self-employed applicants

- Age limit: Self-employed individuals should usually fall within the age range of 21 to 65 years to meet eligibility criteria.

- Minimum income: A minimum annual income, commonly around ₹15 lakh, is required for self-employed applicants. This figure may vary across different lenders.

- Minimum business continuity: Typically, a business continuity of at least 3 years is preferred, though some lenders may stipulate a longer period.

- Credit score

Similar to salaried applicants, self-employed individuals are generally expected to have a credit score of preferably 700 and above for favourable loan terms.

- Loan quantum and tenor can vary widely among NBFCs.

- The amount you can borrow typically ranges from ₹50,000 to ₹75 lakhs.

- The tenure of a regular personal loan usually ranges from 1 year to 5 years.

- However, some lenders offer maximum personal loan tenure for 6 to 8 years

Prerequisites

Income proof

Income proof is essential documentation verifying an individual’s financial stability and repayment capability for a personal loan.- Salary slips, offering a snapshot of regular income.

- Bank account statements of the last 3 months for transcation history.

- Income tax returns for a comprehensive overview of earnings and tax liabilities.

Identity proof

Identity proof is a fundamental requirement in the personal loan application process, establishing the applicant’s true identity.Accepted documents, such as Aadhar Card and Passport, provide official confirmation of the individual’s name, photograph, and essential details, ensuring a secure and legitimate transaction.

Address proof

Address proof validates an applicant’s residential address for a personal loan application.Documents like utility bills, passport, and voter ID serve this purpose, offering tangible evidence of the individual’s place of residence.

Employment certificate

An employment certificate is a formal document from the employer, confirming an individual’s employment status, tenure, and salary details. It strengthens the loan application by providing official validation of the applicant’s income and employment stability, instilling confidence in the lender.Processing time

Personal loans are known for their quick processing.

- Upon submission of your loan application along with the required documents, the lender initiates the approval procedure.

- The timeframe for approval varies depending on the chosen lender, typically ranging from two to three working days, making them an excellent choice for immediate medical expenses.

- If there is a lapse in submitting the correct documents, the approval process may extend beyond this stipulated period.

- The efficiency of the approval process is contingent on both the lender's policies and the timely provision of accurate documentation by the applicant.

Costs

The cost of personal loans can vary depending on the lender, but here are the key components to consider:

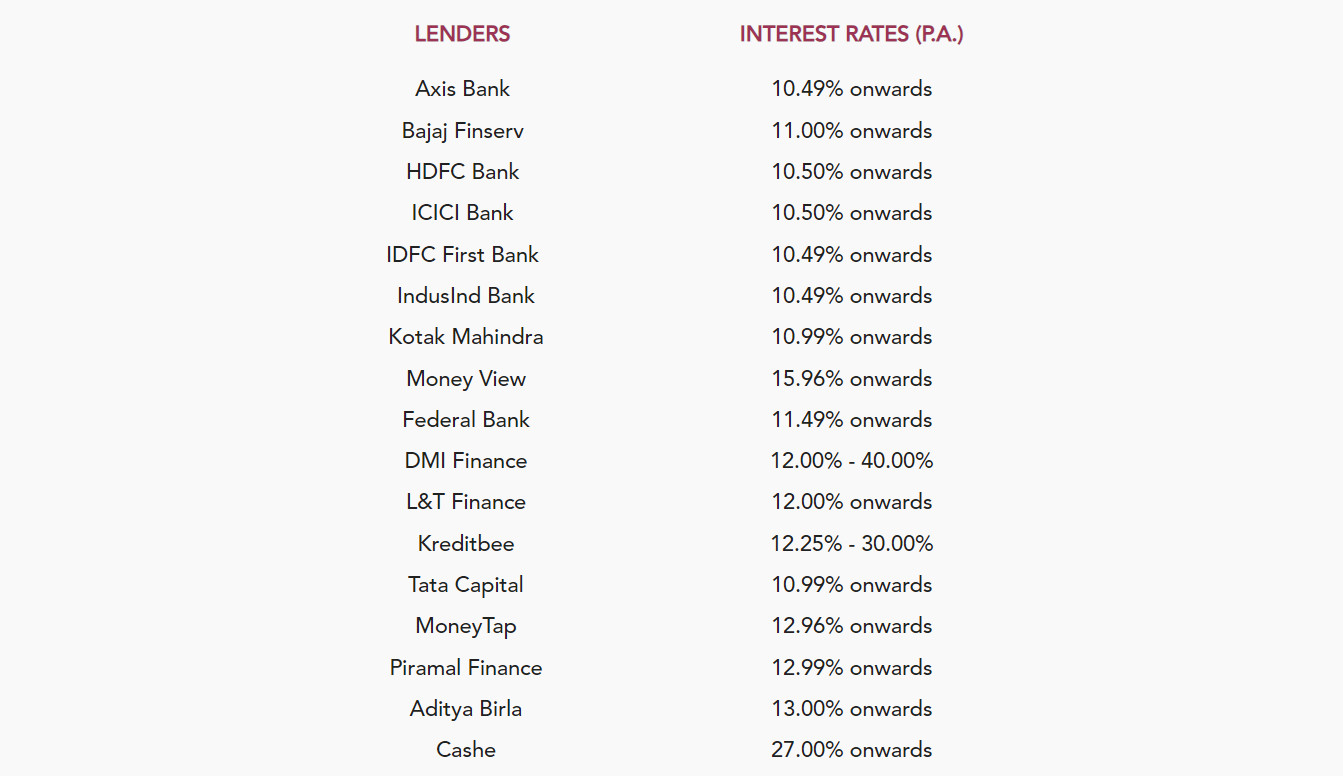

Interest rates

The table above shows the interest rate of various popular loan providers (2023).

Personal loan interest rates in India can fluctuate widely, ranging from 10% to 30% or higher. The actual rate is contingent on the lender’s policies and the borrower’s creditworthiness.

Personal loan interest rates in India can fluctuate widely, ranging from 10% to 30% or higher. The actual rate is contingent on the lender’s policies and the borrower’s creditworthiness.

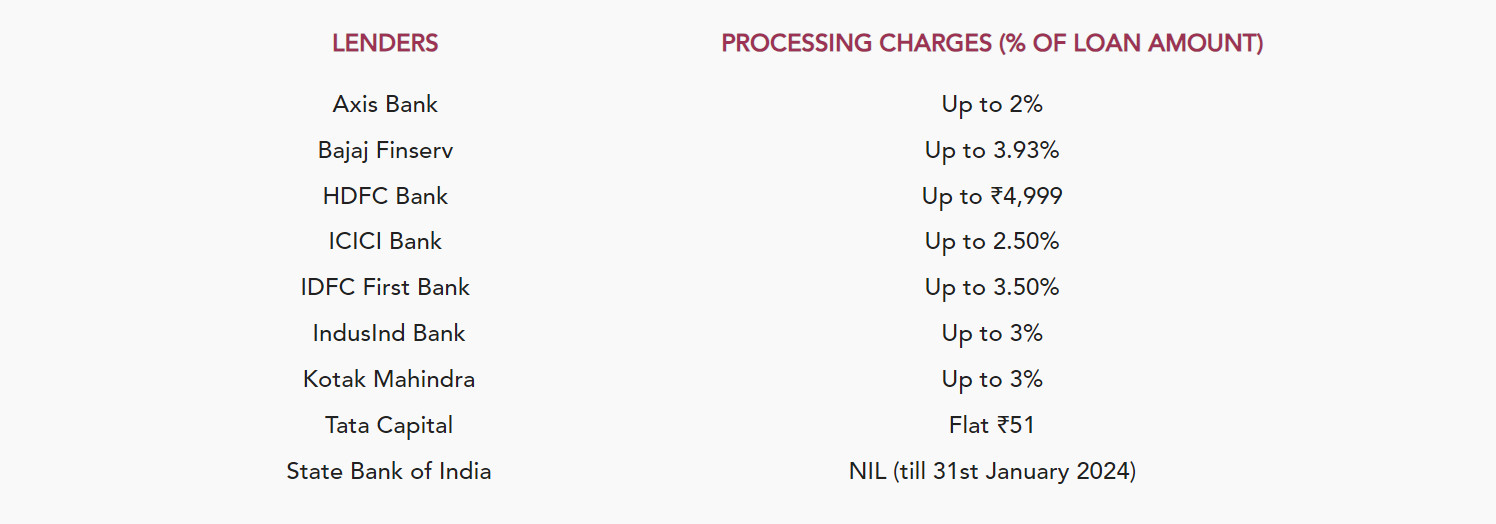

Processing fees

The table above shows the processing fees of various popular loan providers (2023).

Lenders typically impose a processing fee, typically 1-2% of the loan amount. This fee is charged for the administrative tasks involved in handling and approving the loan application.

Lenders typically impose a processing fee, typically 1-2% of the loan amount. This fee is charged for the administrative tasks involved in handling and approving the loan application.

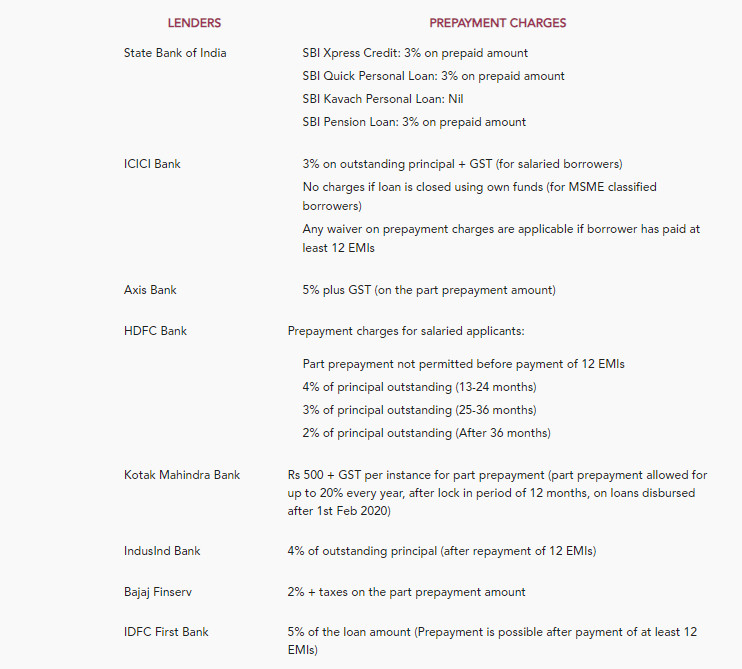

Prepayment charges

The table above shows the prepayment charges of various popular loan providers (2023).

Personal loan prepayment helps borrowers to save on the interest costs that they would have incurred had the loan continued for the entire term.

For example, if a loan applicant wants a personal loan of ₹10 lakh at 13% p.a. interest rate for a 5-year loan tenure, the EMI will be ₹22,753 and the total interest cost will be about ₹3.65 lakhs. If they decide to repay the entire outstanding loan amount after 1 year, they will be able to save around ₹2.44 lakhs in interest costs.

However, Some Non-Banking Financial Companies (NBFCs) may enforce prepayment penalties if borrowers choose to settle the loan before the agreed-upon tenor, impacting the overall cost.

Personal loan prepayment helps borrowers to save on the interest costs that they would have incurred had the loan continued for the entire term.

For example, if a loan applicant wants a personal loan of ₹10 lakh at 13% p.a. interest rate for a 5-year loan tenure, the EMI will be ₹22,753 and the total interest cost will be about ₹3.65 lakhs. If they decide to repay the entire outstanding loan amount after 1 year, they will be able to save around ₹2.44 lakhs in interest costs.

However, Some Non-Banking Financial Companies (NBFCs) may enforce prepayment penalties if borrowers choose to settle the loan before the agreed-upon tenor, impacting the overall cost.

Late payment fees

Failing to adhere to the repayment schedule can result in late payment charges, adding an extra financial burden. It is essential for borrowers to stay vigilant about timely repayments.

Availing a personal loan based on the type of treatment

When contemplating a personal loan for medical expenses, it’s essential to first distinguish between non-elective and elective treatments.

Non-elective treatment

Non-elective treatments are medically necessary interventions for acute conditions, accidents, or serious illnesses that demand immediate attention to prevent significant health risks. Personal loans are often justified for these treatments as they provide a swift source of funds.Elective treatment

Elective procedures are planned medical interventions that are not immediately life-threatening, like cosmetic surgery, fertility treatments, or non-urgent joint replacements. While personal loans can still be used for elective treatments, careful consideration is necessary, as opting to postpone or save for these expenses may be a more financially prudent choice.Availing a personal loan based on patient-borrower relationship

Additionally, when considering a personal loan for medical expenses, it’s important to define the relationship between the patient and the borrower. This distinction can significantly impact the decision.

Patient as borrower

In one scenario, the patient takes on the role of the borrower, applying for a personal loan to cover their own medical expenses. This arrangement is straightforward and allows the patient to independently manage their finances.Patient as borrower

Alternatively, family members, such as parents or spouses, may choose to apply for a personal loan to finance the patient’s treatment in certain situations. In such cases, the lender will evaluate the borrower’s eligibility and creditworthiness. This approach may be suitable when the patient lacks the necessary financial standing to secure a loan.Health insurance coverage

Suppose a cancer patient has health insurance that covers medical expenses related to hospitalization, surgery, and chemotherapy. However, there are certain aspects that insurance may not fully cover, such as:

Non-medical expenses

Personal loans can cover non-medical expenses like travel and accommodation during treatment, which are typically not included in health insurance policies.Advanced treatments

In some cases, insurance may not cover advanced or experimental treatments, but the patient may choose to explore these options. Personal loans can bridge the financial gap for such treatments.Loss of income

During prolonged treatment, the patient or their caregiver may experience a loss of income due to reduced working hours or job loss. Personal loans can provide financial support to cover living expenses during this period.Pros of using personal loans during medical emergencies

Quick access to funds

Personal loans provide rapid access to funds, an invaluable advantage during urgent medical situations where immediate financial support is crucial.No collateral

Being unsecured, personal loans eliminate the need for collateral or security, allowing individuals to secure funds without risking their assetsFlexible usage

The versatility of personal loans extends to their usage, offering borrowers the freedom to allocate funds as needed, whether for hospital bills, surgeries, medications, or post-treatment expenses.Customized tenor

Personal loans often offer a variety of repayment tenors, allowing borrowers to choose a timeframe that aligns with their financial capacity, thereby easing the burden of repayment.Cons of using personal loans during medical emergencies

High interest rates

Despite their convenience, personal loans tend to carry higher interest rates, potentially increasing the overall cost of the borrowed amount over time.Risk of debt

Accumulating additional debt through personal loans poses a financial risk, particularly if the borrower already manages existing financial commitments, potentially leading to a debt cycle.Credit score impact

Defaulting on personal loan payments can have a lasting negative impact on your credit score, affecting your ability to secure favorable terms for future credit.Processing fees

Personal loans may come with processing fees, adding an upfront cost to the borrower that should be considered when assessing the overall affordability of the loan.Limited quantum

The loan amount available through personal loans may be limited, and it may not cover extensive or ongoing medical expenses, necessitating careful consideration of the adequacy of the loan amount for the specific emergency.What to remember before taking a personal loan

By carefully considering these factors, you can make a more informed decision about whether a personal loan is the right choice for your financial situation:

Assess your financial situation

Understand your current financial situation, including your income, expenses, and existing debts. Ensure that you can afford the monthly loan payments without compromising your financial stability.Total cost of the loan

Calculate the total cost of the loan over its entire duration. This includes interest, fees, and any other costs. This will give you a clearer picture of the financial commitment you are making.Check your credit score

A higher credit score often results in lower interest rates. Check your credit score and take steps to improve it if necessary before applying for a loan.Interest rates and fees

Understand your current financial situation, including your income, expenses, and existing debts. Ensure that you can afford the monthly loan payments without compromising your financial stability.Purpose of the loan

Clearly define the purpose of the loan. Whether it’s for debt consolidation, home improvement, education, or other needs, having a specific purpose can help you determine the loan amount and terms.Loan terms

Carefully review the loan terms, including the repayment period and any associated penalties for early repayment. Longer loan terms may result in lower monthly payments but could cost more in interest over the life of the loan.Secured vs unsecured loan

Personal loans can be either secured (backed by collateral) or unsecured. Secured loans may have lower interest rates, but they carry the risk of losing the collateral if you default on the loan.Read the fine print

Carefully read and understand the terms and conditions of the loan agreement. Pay attention to any clauses related to prepayment penalties, late fees, or other terms that may impact the cost of the loan.Repayment plan

Have a clear plan for repaying the loan. Ensure that the monthly payments fit comfortably within your budget. Consider creating an emergency fund to cover unexpected expenses and prevent financial strain.Consider alternatives

Before committing to a personal loan, explore other financing options such as credit cards, home equity loans, or lines of credit. Each option has its advantages and disadvantages.Lender reputation

Choose a reputable lender with a history of fair and transparent lending practices. Read reviews, check the lender’s ratings, and gather feedback from other borrowers.Future financial goals

Consider how taking a personal loan aligns with your long-term financial goals. Will it help you achieve your objectives, or could it hinder your financial progress?How Milaap can help

Taking a personal loan for medical bills can provide immediate relief, but it’s important to weigh the long-term financial impact, including interest rates and repayment terms. Before committing to a loan, consider all available options, including government schemes, insurance coverage, and financial assistance from NGOs.

If these options are insufficient or unavailable, Milaap offers an alternative solution. By starting a fundraiser on Milaap, you can receive support from friends, family, and a wider community to cover medical treatment costs without the burden of debt. If you're facing high medical expenses, consider Milaap as a way to ease the financial strain and focus on recovery.

Please note: This information is for general purposes only and is not financial or legal advice.

The details and costs presented are subject to change due to various factors, such as regulatory updates, economic conditions, and individual circumstances. Relying on this information is at the reader’s own risk, and it is advisable to consult with financial experts for accurate and up-to-date information tailored to individual circumstances.

If these options are insufficient or unavailable, Milaap offers an alternative solution. By starting a fundraiser on Milaap, you can receive support from friends, family, and a wider community to cover medical treatment costs without the burden of debt. If you're facing high medical expenses, consider Milaap as a way to ease the financial strain and focus on recovery.

Please note: This information is for general purposes only and is not financial or legal advice.

The details and costs presented are subject to change due to various factors, such as regulatory updates, economic conditions, and individual circumstances. Relying on this information is at the reader’s own risk, and it is advisable to consult with financial experts for accurate and up-to-date information tailored to individual circumstances.